- US trade groups asked the Consumer Financial Protection Bureau to pause crackdown on overdraft fees.

- A growing number of incumbents are already adding or proactively promoting alternative liquidity-assistance services.

The news: US financial-services trade groups led by the American Bankers Association (ABA) asked the Consumer Financial Protection Bureau (CFPB) to pause its pending crackdown on overdraft fees, arguing that it could deprive consumers of an option to avoid falling behind on their personal expenses. In the meantime, they want the regulator to gather insights into frequent-overdraft users.

More on this: At stake is a revenue source that brought in $8.82 billion for banks during 2020, per S&P Global Market Intelligence.

The associations contend that restricting overdraft-related items will leave some people worse off because they will lose access to a solution that helps them manage their short-term liquidity—potentially leading to:

- An increase in declined transactions and returned checks.

- Fees from merchants and landlords.

- Hits to credit ratings.

- Requirements to use money orders or other payment methods.

The groups also pointed to public opinion data in making their case, such as:

- A 2021 survey from Curinos that found 62% of respondents said they would reconsider their support for regulations if it resulted in limited overdraft access.

- A Morning Consult survey showing that three in four respondents were happy that their overdrafted payments were covered. The October 2021 survey was commissioned by the ABA, and also found that 62% replied that charging for overdraft protection is reasonable.

The trade organizations also pointed to measures that financial institutions are already taking to reduce consumers' overdraft-fee exposure, such as 24-hour grace periods letting people eliminate their negative balances, early access to direct deposits, and being able to link their transaction accounts to outside sources of funds.

Anti-exposure measures have been recently added by a series of big incumbent banks, such as Wells Fargo, Bank of America, and JPMorgan Chase.

What do the associations want? They called on the CFPB to study consumers' overdraft preferences and collect data, including:

- What times and needs typically lead consumers to overdraft.

- Whether protection from overdrafts has helped consumers avoid late fees, hardships like evictions, or utility shut-offs.

- Whether they are aware of alternatives for covering their overdrafts, or have taken advantage of them.

- Why people opt for overdraft protection versus other options available.

The big takeaway: While the trade groups' request that the CFPB gather insights on consumers' motives and awareness is reasonable, legally curtailing overdraft fees won't necessarily push people into trading one hardship for another.

A growing number of incumbents are already adding or proactively promoting alternative liquidity-assistance services, such as:

- Short-term loans for small amounts.

- Making existing anti-overdraft measures more convenient by dropping transfer fees from outside accounts.

- Grace periods and early access to direct deposits.

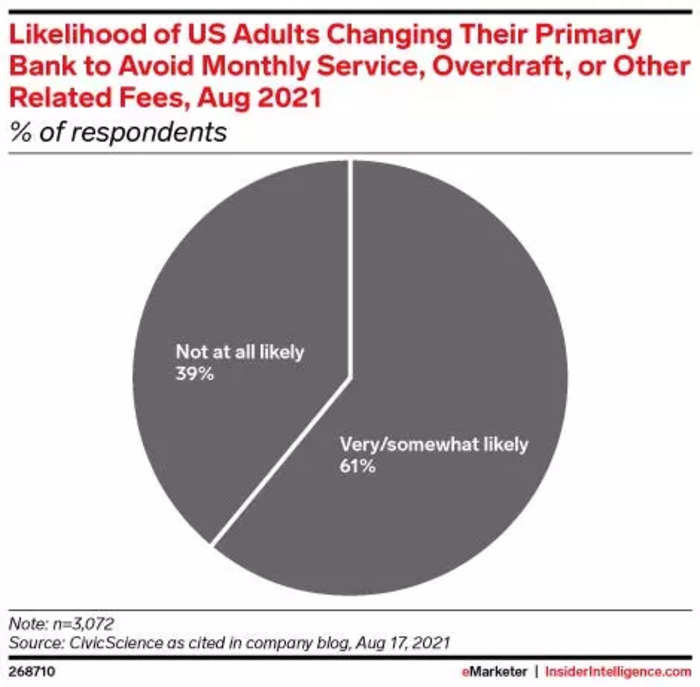

Consumers are not necessarily enthusiastic about overdraft fees, notwithstanding the question about whether they are reasonable.

- Banking giant Truist—which this week unveiled two no-fee accounts and anti-exposure measures—noted that it made these changes after gathering input from its customers.:

- Survey data from Morning Consult that was highlighted this month found that people who rely on overdrafting were more than twice as likely to be receptive to starting a relationship with a different financial institution within the next six months.

- A June 2021 survey from the company also showed divided sentiment on the practice, with 52% viewing fees as unfair and 48% viewing them as fair.

Want to read more stories like this one? Here's how you can gain access:

- Join other Insider Intelligence clients who receive Banking forecasts, briefings, charts, and research reports to their inboxes each day. >> Become a Client

- Explore related topics more in depth. >> Browse Our Coverage

Current subscribers can access the entire Insider Intelligence content archive here.

Next Story

Next Story I spent 2 weeks in India. A highlight was visiting a small mountain town so beautiful it didn't seem real.

I spent 2 weeks in India. A highlight was visiting a small mountain town so beautiful it didn't seem real.  I quit McKinsey after 1.5 years. I was making over $200k but my mental health was shattered.

I quit McKinsey after 1.5 years. I was making over $200k but my mental health was shattered. Some Tesla factory workers realized they were laid off when security scanned their badges and sent them back on shuttles, sources say

Some Tesla factory workers realized they were laid off when security scanned their badges and sent them back on shuttles, sources say World Liver Day 2024: 10 Foods that are necessary for a healthy liver

World Liver Day 2024: 10 Foods that are necessary for a healthy liver

Essential tips for effortlessly renewing your bike insurance policy in 2024

Essential tips for effortlessly renewing your bike insurance policy in 2024

Indian Railways to break record with 9,111 trips to meet travel demand this summer, nearly 3,000 more than in 2023

Indian Railways to break record with 9,111 trips to meet travel demand this summer, nearly 3,000 more than in 2023

India's exports to China, UAE, Russia, Singapore rose in 2023-24

India's exports to China, UAE, Russia, Singapore rose in 2023-24

A case for investing in Government securities

A case for investing in Government securities