MORGAN STANLEY: Buy these 25 growth stocks to profit from huge gains, even if the global economy tanks

1. Adobe

Ticker: ADBE

12-month performance: 41%

Comment: "Adobe is participating in a ~$108B total addressable market (TAM) with strong secular tailwinds around digital content creation, digital marketing,and eCommerce," Keith Weiss said.

"As Adobe integrates recent acquisitions of Marketo and Magento into an already rich product portfolio, we see the possibility for the company to widen its competitive moat. Together, we see these secular forces supporting both revenue and above-market EPS growth."

Source: Morgan Stanley

2. Alphabet

Ticker: GOOGL

12-month performance: 5.5%

Comment: "As the dominant player in paid search, Google continues to benefit from secular growth as advertising dollars shift into digital," Brian Nowak said.

"Google also owns YouTube, the leader in online video advertising, an industry we believe will grow by nearly 25% from 2017 to 2020 to ~$22bn in the US alone."

Source: Morgan Stanley

3. Amazon

Ticker: AMZN

12-month performance: 44%

Comment: "As the dominant player in US eCommerce, Amazon continues to experience secular growth as retail dollars shift online," Nowak said.

"As Amazon scales its logistics network and expands its Prime membership program globally, we see a significant opportunity to capture a larger piece of the ~$1tn worldwide eCommerce market (ex China)."

Source: Morgan Stanley

4. Assurant

Ticker: AIZ

12-month performance: -3.3%%

Comment: "AIZ’s fee-based and extended warranty businesses (renters, vehicle, and smart phone) should see strong revenue growth, thanks to increasing consumer demand, higher take-up rates, and expanding partnerships," Kai Pan said.

"Its recent acquisition of The Warranty Group broadens its distribution partners and its global presence, helping to drive more revenue growth."

Source: Morgan Stanley

5. Atlassian

Ticker: TEAM

12-month performance: 83%

Comment: "In our view,an expanding solution portfolio and strong value proposition positions Atlassian for durable 30%+ revenue growth, on the back of: 1) continued expansion of the customer base, 2) further penetration into existing customers, and 3) exerting pricing power with ongoing price hikes," Weiss said.

Source: Morgan Stanley

6. BioMarin Pharmaceutical

Ticker: BMRN

12-month performance: 16.8%

Comment: "We believe the strong base business, which generated ~$1.3B in sales in 2017, coupled with a diverse and promising pipeline that could generate blockbuster drugs makes BioMarin a unique large cap biotech story," Matthew Harrison said.

"Key secular tailwinds for BioMarin, in our view, include a low probability of generic/biosimilar competition to BioMarin’s base business and a deep and wide pipeline with drugs that could launch by 2020."

Source: Morgan Stanley

7-8. Booking Holdings and Expedia

12-month performance: 9% (BNKG), -2% (EXPE)

Comment: "As the leading players in online travel, Booking and Expedia continue to benefit from secular growth as travel dollars shift online," Nowak said.

"The $1.3 trillion global travel industry remains a highly fragmented market and both BKNG and EXPE look well positioned given their scale advantages and portfolio of brands. In all, over the next 3 years we expect BKNG’s gross bookings to grow at a 13% CAGR and EXPE’s at an 11% CAGR."

Source: Morgan Stanley

9. Illumina

Ticker: ILMN

12-month performance: 50%

Comment: "As the dominant provider of technology to sequence DNA, ILMN stands to benefit from a series of market developments and policy changes that have emerged over the last year," Steve Beuchaw said.

"1) The success of DNA-driven drug administration in immunotherapy by Merck ... 2) Global pharma and government funding for DNA analysis has a stronger growth outlook ... 3) Consumer interest in DNA-derived applications has inflected, evidenced by the 300%+ growth in consumer test orders over the last 2 years. 4) Growing global research funding, with an ongoing mix shift towards genomic research."

Source: Morgan Stanley

10. Intuitive Surgical

Ticker: ISRG

12-month performance: 32%

Comment: "Intuitive Surgical is the leader in robotic surgery," David Lewis said.

"The company has gained significant adoption within urology and gynecology and is still in the relatively early stages of penetration internationally and within broader procedures (including general surgery)."

Source: Morgan Stanley

11. IQVIA

Ticker: IQV

12-month performance: 32%

Comment: "We believe IQVIA’s unique data assets, therapeutics expertise,and scale differentiate the company relative to other contract research organizations (CROs) and positions it to service pharma manufacturers as drug development increasingly becomes digitalized," Ricky Goldwasser said.

"Over time, IQVIA should benefit from the FDA’s increased focus on modernizing clinical trials design, which has the potential to be a game-changer for biopharma companies, CROs, and new entrants from the technology side."

Source: Morgan Stanley

12. MasterCard

Ticker: MA

12-month performance: 33%

Comment: "MA's compounding growth drivers include (i) strong global consumer spending, (ii) market share gains, and (iii) the secular shift to card from cash," James Faucette said.

"As the second-largest global card network (behind Visa), MA is well positioned to benefit from market share gains in particular regions and consumer spending trends, which have been fairly resilient even through economic cycles."

Source: Morgan Stanley

13. National Vision

Ticker: EYE

12-month performance: 33%

Comment: "We believe EYE offers a unique blend of defensiveness and growth vis-À-vis its focus on value within the non-cyclical optical retail segment and ~50% unit growth runway," Simeon Gutman said.

"EYE has delivered 67 consecutive quarters of positive SSS and is expected to grow square footage ~10% annually over the next several years."

Source: Morgan Stanley

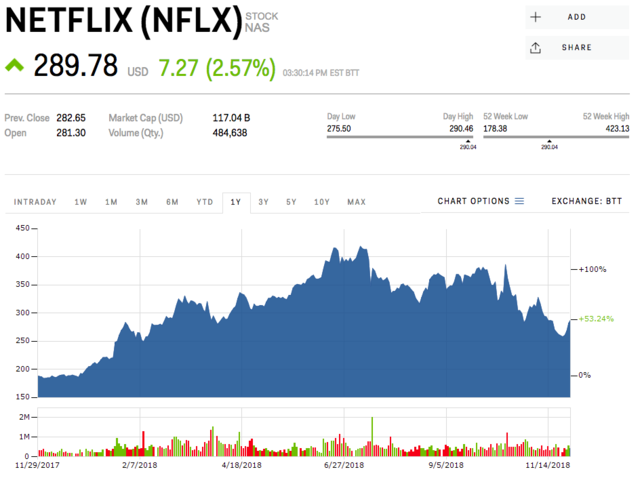

14. Netflix

Ticker: NFLX

12-month performance: 53%

Comment: "Proven success in the US and initial international markets provides a roadmap for success in newer markets, with scale and innovation providing Netflix the ability to drive margin expansion," Benjamin Swinburne said.

"Growth in global broadband penetration should increase Netflix’s addressable market, driving member growth and providing further opportunity for Netflix to expand in new geographies."

Source: Morgan Stanley

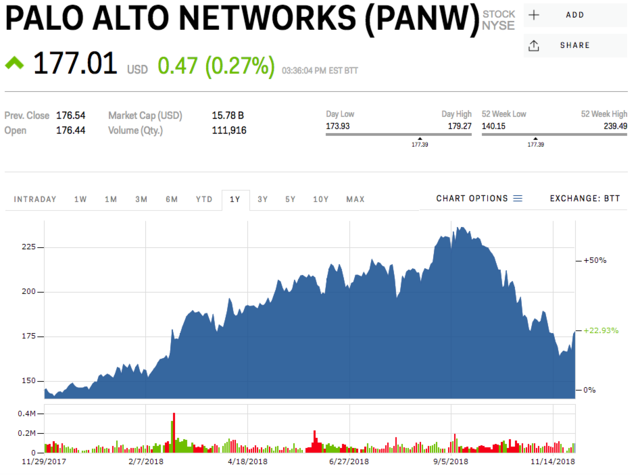

15. Palo Alto Networks

Ticker: PANW

12-month performance: 23%

Comment: "In order to garner more effectiveness and efficiency in information security architectures, we believe the key secular trend in security will be the consolidation of spending towards integrated security platforms," Weiss said.

"Palo Alto Networks stands well positioned to excel within that trend given its leadership in core network security and growing traction into areas such as Endpoint, Cloud,and Security Analytics."

Source: Morgan Stanley

16. Pluralsight

Ticker: PS

12-month performance: 19%

Comment: "We believe Pluralsight is well positioned to help enterprises address the need for IT knowledge while managing an accelerating industrywide talent gap," Brian Essex said.

"Pluralsight offers what we see as a best-in class IT-focused Learning Management Software platform to address this need. The platform is driven by machine learning technology that not only enables a more efficient learning process at the individual level but also enables enterprises to efficiently quantify, develop,and manage talent across technology platforms."

Source: Morgan Stanley

17. Regeneron Pharmaceuticals

Ticker: REGN

12-month performance: 0.6%

Comment: "Regeneron is a diversified large cap biotech company, with commercialized drugs focusing on ophthalmology, atopic dermatitis, asthma, cardiology, and oncology," Matthew Harrison said.

"Ophthalmology drug Eylea generated ~$3.7B in 2017 for Regeneron,and we expect the drug to remain steady through the mid-2020Es, generating ~$4B in sales for Regeneron by 2025E."

Source: Morgan Stanley

18. Salesforce.com

Ticker: CRM

12-month performance: 0.3%

Comment: "With direct participation in key software themes including machine learning, mobile, internet of things, and cloud computing broadly, we believe Salesforce.com remains one of the best secularly positioned names in tech," Weiss said.

"An estimated $200B+ potential market opportunity and $21B of billed and unbilled backlog provides CRM ample runway for 20%+ revenue growth and a 30%+ FCF CAGR through FY24, in our view."

Source: Morgan Stanley

19. ServiceNow

Ticker: NOW

12-month performance: 48%

Comment: "Emerging as one of the premier Software as a Service (SaaS) vendors, we see ServiceNow sustaining both topline momentum and garnering further FCF leverage from its building subscription base," Weiss said.

"Breaking out of its core market in IT (an ~$10B opportunity), ServiceNow addresses a broader opportunity of workflow automation across the entire enterprise ($45B opportunity)."

Source: Morgan Stanley

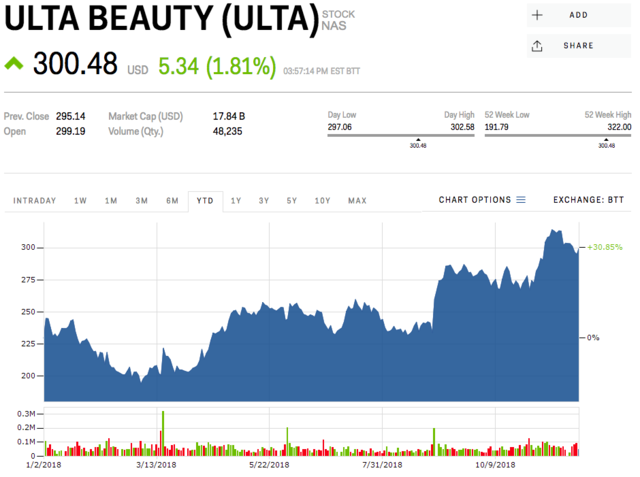

20. Ulta Beauty

Ticker: ULTA

12-month performance: 38%

Comment: "We argue that ULTA is one of a few retailers with store growth (+8% in 2019), expanding gross profit pools,and improving EBIT margins, enabling the business to compound earnings over time," Simeon Gutman said.

"This stands in stark contrast to many retailers that are delivering 'profitless growth' characterized by decent SSS growth but declining EBIT dollars and margins."

Source: Morgan Stanley

21. Veeva Systems

Ticker: VEEV

12-month performance: 68%

Comment: "Veeva started out as a purely vertical provider of SaaS-based Sales Force Automation tools, and is now actively working to parlay its leadership position in Life Sciences toward expansion into adjacent verticals," Stan Zlotsky said.

"With a number of early customer wins, Veeva has greatly expanded its addressable market (TAM) from $5B at IPO to $9B+ today,according to management."

Source: Morgan Stanley

22. Vertex Pharmaceuticals

Ticker: VRTX

12-month performance: 68%

Comment: "Vertex is a biotech company that focuses primarily on cystic fibrosis (CF)," Matthew Harrison said.

"The company’s CF therapies Kalydeco and Orkambi collectively generated ~$2.2B in sales in 2017, and a third therapy (Symdeko) was approved in early 2018, which we believe could generate ~$750M in sales for 2018E. Furthermore, Vertex is developing a triple combination therapy that has generated strong late-stage data and could address a large portion of the CF market."

Source: Morgan Stanley

23. Visa

Ticker: V

12-month performance: 27%

Comment: "Visa is a key beneficiary of robust consumer spending worldwide, the ongoing migration from cash to electronic payments, and broadening merchant acceptance," Faucette said.

"Global Personal Consumption Expenditure and secular growth drivers should support high-single digit volume growth and low double-digit revenue growth in the near-to-medium term."

Source: Morgan Stanley

24. Workday

Ticker: WDAY

12-month performance: 46%

Comment: "We believe the Workday story yields multiple dimensions for sustaining strong top-line growth, combined with best in class unit economics, should drive margins significantly higher, resulting in strong FCF growth long-term," Weiss said.

"With a cloud platform encompassing the Human Capital Management (HCM), Payroll, Financial Accounting, Financial Planning, and Business Intelligence markets, Workday directly addresses some of the largest areas of spend in application software resulting in an addressable opportunity that we estimate has increased from ~$40B at the time of its IPO to ~$80B today."

Source: Morgan Stanley

25. Zoetis

Ticker: ZTS

12-month performance: 30%

Comment: "We believe Zoetis has a combination of compelling organic growth, franchise durability, margin expansion potential, improving cash flow conversion, and tuck-in M&A optionality," David Risinger said.

"Favorable mega-trends include rising global demand for protein consumption, increased pet ownership and better care for Companion Animals (primarily dogs and cats)."

Source: Morgan Stanley

Next Story

Next Story I quit McKinsey after 1.5 years. I was making over $200k but my mental health was shattered.

I quit McKinsey after 1.5 years. I was making over $200k but my mental health was shattered. Some Tesla factory workers realized they were laid off when security scanned their badges and sent them back on shuttles, sources say

Some Tesla factory workers realized they were laid off when security scanned their badges and sent them back on shuttles, sources say I tutor the children of some of Dubai's richest people. One of them paid me $3,000 to do his homework.

I tutor the children of some of Dubai's richest people. One of them paid me $3,000 to do his homework.

5 things to keep in mind before taking a personal loan

5 things to keep in mind before taking a personal loan

Markets face heavy fluctuations; settle lower taking downtrend to 4th day

Markets face heavy fluctuations; settle lower taking downtrend to 4th day

Move over Bollywood, audio shows are starting to enter the coveted ‘100 Crores Club’

Move over Bollywood, audio shows are starting to enter the coveted ‘100 Crores Club’

10 Powerful foods for lowering bad cholesterol

10 Powerful foods for lowering bad cholesterol

Eat Well, live well: 10 Potassium-rich foods to maintain healthy blood pressure

Eat Well, live well: 10 Potassium-rich foods to maintain healthy blood pressure