Here’s why analysts are saying Manyavar’s IPO is heavily expensive leaving very little room for investor profit

Feb 2, 2022, 17:09 IST

- Vedant Fashions, owner of ethnic wear brand Manyavar, is all set to open its IPO from February 4 at ₹824-866 per share.

- Shares of the company are already demanding a premium of ₹40 per share in the grey market.

- However, analysts are not very confident about the company maintaining its profit levels in the coming years because of high margin and inflation pressure.

Advertisement

If you are looking to invest in the upcoming initial public offering (IPO) of ethnic wear brand ‘Manyavar’, then you may want to know what analysts are suggesting before investing.Kolkata-based Vedant Fashions, which owns ethnic wear brand Manyavar, will open its IPO on February 4 and will close on February 8.

The ethnic wear company sells its products through five brands -- Manyavar, Mohey, Mebaz, Manthan and Twamev. The company’s flagship brand ‘Manyavar’ is one of the famous brands known for wedding collections.

However, buying clothes from a famous brand is not similar to buying shares of the same company.

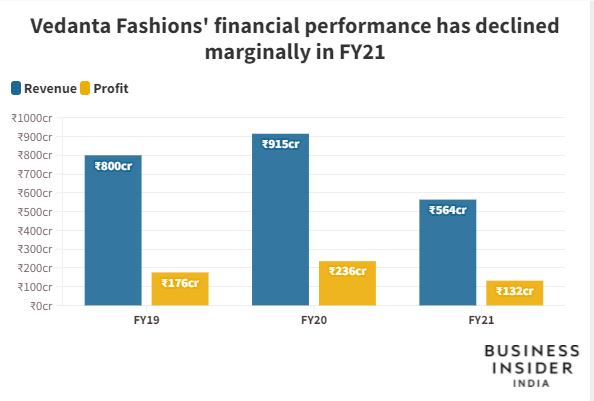

Before moving ahead, here’s how the company’s financials have behaved in the past three years.

Advertisement

Moreover, analysts are not very confident about the company maintaining its profit levels in the coming years because of high margin and inflation pressure.

While Vedant Fashions gets pricing power over its products as the Indian wedding and celebration wear market is relatively less price-sensitive, pressure to maintain a high margin above 40% seems challenging, say analysts at Choice Broking.

Analysts believe it is difficult to “maintain (margins) given the competition from the local retailers, online retailers and non-branded products and building inflationary pressure. Furthermore, business is highly concentrated on wedding and festival wear and thereby vulnerable to variations in demand.”

“Thereby, we view the issue is aggressively priced leaving no margin of safety for investors,” said the report by the broking firm while it assigned ‘Subscribe with Caution’ rating for the IPO.

Advertisement

A report by Anand Rathi Research pointed out risks like mounting competition in men’s celebration wear from Aditya Birla Fashion and Retail, Reliance, etc., keen competition in women’s celebration wear and slow-down in consumption.| Listed peers | Market cap | Share price as of Feb 2 |

| Page Industries | ₹48,262 crore | ₹43,269 |

| Aditya Birla Fashion & Retail | ₹28,978 crore | ₹308 |

| Trent | ₹24,512 crore | ₹1,094 |

| Vedant Fashions | ₹21,017 crore | ₹866 |

| Lux Industries | ₹8,641 crore | ₹2,877 |

| V-Mart Retail | ₹7,373 crore | ₹3,735 |

| Go Fashion | ₹5,638 crore | ₹1,044 |

| Raymond | ₹5,115 crore | ₹768 |

| TCNS Clothing | ₹4,589 crore | ₹745 |

| Arvind Fashions | ₹4,226 crore | ₹319 |

| Rupa Company | ₹4,134 crore | ₹519 |

| Shoppers Stop | ₹4,066 crore | ₹371 |

| Kewal Kiran Clothing | ₹1,419 crore | ₹230 |

SEE ALSO: Meet Maju Kuruvilla, the new Indian-origin CEO of fintech startup Bolt

More employees are leaving Tech Mahindra than TCS and Wipro