Only one-third of Yes Bank’s customers withdrew more than the ₹50,000 during the moratorium period, according to Yes Bank administrator Prashant Kumar.

He also noted that there has been more inflow than outflow of funds during the last four days.

The moratorium placed on the troubled private bank by the Reserve Bank of India (RBI) will end tomorrow, March 18, at 6:00 pm.

India’s troubled private bank Yes Bank is scheduled to open up to customers tomorrow after the moratorium placed by the Reserve Bank of India (RBI) comes to an end. Prashant Kumar — former SBI deputy managing director who was instituted as the administer of Yes Bank by the RBI — believes that things are turning around for the better.

“In the last four days, we had higher inflows than outflows,” he said during a press conference today, March 17. He also pointed out that only one-third of Yes Bank’s customers withdrew more than ₹50,000 since the moratorium came into effect on March 5.

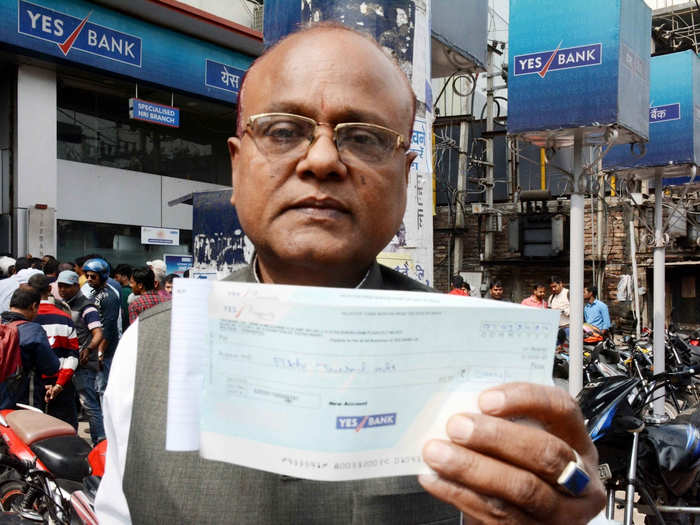

People lined up outside Yes Bank to withdraw cash after RBI announced the one-month moratoriumIANS

The Yes Bank moratorium will lift on March 18 at 6:00 pm. Yesterday, March 16, the RBI governor told depositors that there is no rush to withdraw funds from their accounts.

“The depositor’s money is absolutely safe. There is no reason for undue worry. This is no need for rushing into withdrawing their deposits or their money which is with Yes Bank,” he said.

Advertisement

The one-month moratorium comes to an end

Once the moratorium is lifted on March 16, Kumar will be leading the board as chief executive and managing director of Yes Bank. Along with him, Sunil Mehta — former non-executive chairman of Punjab National Bank (PNB) — will be the non-executive chairman of Yes Bank and Mahesh Krishnamurthy will serve as the non-executive director.

The moratorium placed a ₹50,000 cap on all withdrawals from Yes Bank. Das lauded Yes Bank’s restructuring scheme as the “first of its time” with public and private banks partnering up to rescue another bank.

“In India — on earlier occasions, when there was the failure of a scheduled commercial bank — the usual method has been the amalgamation of the failed bank with a larger entity. This time we have not done so. The identity of Yes Bank is retained and the investors are the banks which have come forward,” said Das.

“Never in the banking history of India, depositors have lost money. Their interests have always been protected. The present scheme also protects the interest of depositors,” he added.

NewsletterSIMPLY PUT - where we join the dots to inform and inspire you. Sign up for a weekly brief collating many news items into one untangled thought delivered straight to your mailbox.

Next Story

Next Story Colon cancer rates are rising in young people. If you have two symptoms you should get a colonoscopy, a GI oncologist says.

Colon cancer rates are rising in young people. If you have two symptoms you should get a colonoscopy, a GI oncologist says. I spent $2,000 for 7 nights in a 179-square-foot room on one of the world's largest cruise ships. Take a look inside my cabin.

I spent $2,000 for 7 nights in a 179-square-foot room on one of the world's largest cruise ships. Take a look inside my cabin. An Ambani disruption in OTT: At just ₹1 per day, you can now enjoy ad-free content on JioCinema

An Ambani disruption in OTT: At just ₹1 per day, you can now enjoy ad-free content on JioCinema In second consecutive week of decline, forex kitty drops $2.28 bn to $640.33 bn

In second consecutive week of decline, forex kitty drops $2.28 bn to $640.33 bn

SBI Life Q4 profit rises 4% to ₹811 crore

SBI Life Q4 profit rises 4% to ₹811 crore

IMD predicts severe heatwave conditions over East, South Peninsular India for next five days

IMD predicts severe heatwave conditions over East, South Peninsular India for next five days

COVID lockdown-related school disruptions will continue to worsen students’ exam results into the 2030s: study

COVID lockdown-related school disruptions will continue to worsen students’ exam results into the 2030s: study

India legend Yuvraj Singh named ICC Men's T20 World Cup 2024 ambassador

India legend Yuvraj Singh named ICC Men's T20 World Cup 2024 ambassador