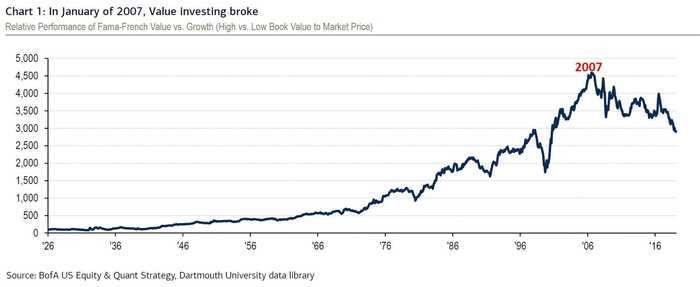

- The near century-long trend of value investing outperforming growth investing has been broken since 2007, according to Bank of America.

- Growth strategies have outperformed value strategies by nearly 8 percentage points since 2007, and that spread has widened even more in 2020 as growth stocks led by the tech sector have materially outperformed value stocks.

- In a note published on Monday, Bank of America highlighted seven reasons why value might finally be poised for a comeback after 13 years of underperformance.

- The bank also played devil's advocate and listed three reasons why growth may continue its decade-long winning trend.

- Visit Business Insider's homepage for more stories.

Value investing is broken. At least, it has been relative to growth since 2007, according to a Bank of America note published Monday.

The bank noted that from 1926 to now, value investing has handily outperformed growth investing, notching a gain of 1,344,600% versus growth's gain of 626,600% over that same time period.

But since the start of 2007, this trend has reversed and growth investing strategies have handily outperformed value investing strategies by nearly 8 percentage points, according to the bank.

"Moreover, outperformance of growth stocks this year has hit all-time highs just in the first half. Growth index returns' spread (26ppt) is higher than during the entire year of 1999, right before the tech bubble burst," BofA said.

Here are seven reasons why value investing may be poised for a comeback, according to the note.

Read more: A Wall Street investment chief dispels the notion that surging stocks are disconnected from the economy — and lays out 3 reasons why the market will continue to climb over the next year

1. "It's the economy, stupid."

Since 1929, every time the US went through a recession, value stocks outperformed the S&P 500 for at least three months around the absolute low of the economic pullback, according to BofA. Additionally, the outperformance by value tends to be wide during the first three months of outperformance, leading on average by 12 percentage points.

2. "Style cycles are driven by profits, not rates."

"When growth is scarce, investors will pay up for growth. As growth broadens out, investors become more price sensitive and seek out the cheapest growth they can find," BofA said. The bank also argued that interest rates "have very little impact on style rotations," according to the note.

3. "Positioning favors value."

There is a near overweight in growth stocks by portfolio managers and investors, which corresponds with a near record underweight in value stocks. Contrarian investors who believe in "reversion to the mean" are likely salivating at the current positioning data. BofA added that anecdotally, its clients "have been aggressive buyers of growth ETFs."

4. "Value is undervalued."

Value stocks trade at a near record discount relative to momentum stocks, "two standard deviations cheap," BofA said. Value has only been this cheap since 2003 and 2008, "after which value outperformed momentum by 22ppt and 69ppt, respectively, over the subsequent 12 months."

5. "Abundance of mean-reversion alpha."

A wide dispersion in valuations between growth and value stocks usually precedes value cycles. "When valuation dispersion has been this high or higher, value stocks have outperformed growth 95% of the time over the subsequent 12 months," BofA highlighted.

6. "Anti-monopolistic risks to growth stocks."

US oligopoly power has risen since 1998 while the number of firms has dropped considerably, BofA noted. The implications for oligopolies, which tend to be growth stocks, not value stocks, are more regulation and higher taxes, lower valuations due to regulatory risk and a drop in profit growth, and in some cases an eventual break-up of some companies, according to the bank.

7. "Japanification favors value."

If the US "becomes Japan," value stocks are poised to outperform. While BofA doesn't think that will happen, it did observe that during Japan's "lost decade" in the 1990s, "value was the best performing factor among the standard quantitative strategies," the note said.

Next, BofA played devil's advocate and countered with three reasons why growth may be poised to continue outperforming value.

Read more: UBS says buy these 18 diamond-in-the-rough stocks that will offer massive gains over multiple years, even as their underlying industries suffer

1. "ESG favors growth."

"Most ESG scoring systems favor tech (growth) and penalize energy (value)," BofA said. With more and more cash flowing into ESG funds, growth stocks stand to be the beneficiary over value stocks. BofA noted that the timing of fund flows into ESG funds aligns with the timeline of when growth started to outperform value: in the late 2000s.

2. "QE Infinity & weak economy favors growth."

Low interest rates benefit "long duration" themes like private equity and secular, rather than cyclical, growth, BofA said. The expansion of the Fed's balance sheet has coincided with the rise of FANG stocks as a percentage of the S&P 500, according to the note. As long as financial conditions remain easy, it's difficult to see the current trend of growth outperforming value reversing.

3. "In some cases, value = melting ice cubes."

"In almost every industry, disruption is evident - new technology disintermediating old business models, creating obsolescence risk. Recall, buggy whips grew incredibly inexpensive before they went to zero," BofA said.

Next Story

Next Story Colon cancer rates are rising in young people. If you have two symptoms you should get a colonoscopy, a GI oncologist says.

Colon cancer rates are rising in young people. If you have two symptoms you should get a colonoscopy, a GI oncologist says. I spent $2,000 for 7 nights in a 179-square-foot room on one of the world's largest cruise ships. Take a look inside my cabin.

I spent $2,000 for 7 nights in a 179-square-foot room on one of the world's largest cruise ships. Take a look inside my cabin. An Ambani disruption in OTT: At just ₹1 per day, you can now enjoy ad-free content on JioCinema

An Ambani disruption in OTT: At just ₹1 per day, you can now enjoy ad-free content on JioCinema In second consecutive week of decline, forex kitty drops $2.28 bn to $640.33 bn

In second consecutive week of decline, forex kitty drops $2.28 bn to $640.33 bn

SBI Life Q4 profit rises 4% to ₹811 crore

SBI Life Q4 profit rises 4% to ₹811 crore

IMD predicts severe heatwave conditions over East, South Peninsular India for next five days

IMD predicts severe heatwave conditions over East, South Peninsular India for next five days

COVID lockdown-related school disruptions will continue to worsen students’ exam results into the 2030s: study

COVID lockdown-related school disruptions will continue to worsen students’ exam results into the 2030s: study

India legend Yuvraj Singh named ICC Men's T20 World Cup 2024 ambassador

India legend Yuvraj Singh named ICC Men's T20 World Cup 2024 ambassador