UK adoption of digital-only challenger banks is currently paltry: Fewer than one in 10 British consumers are using mobile-only banks to manage their money, according to survey data from YouGov.

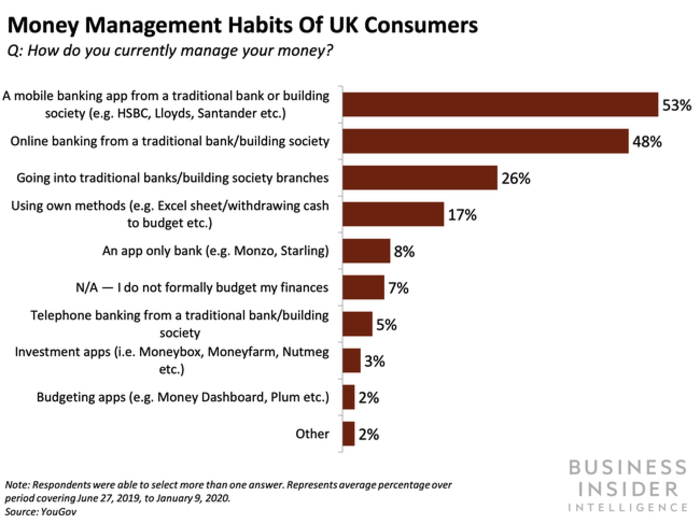

However, this apathy doesn't extend to all forms of digital banking, as British consumers appear inclined to use digital banking offerings from their traditional banks. A majority (53%) of respondents say that they use a mobile banking app from a traditional bank or building society, while 48% say that they use an online banking offering from a traditional bank or building society.

The relatively solid use of digital banking in general suggests that the big challenge for neobanks is not converting consumers to digital platforms, but getting consumers to give digital-only banking a try. Less than one-quarter (23%) of UK consumers are actually uncomfortable with online banking services, per YouGov data, leaving the neobank business model with a strong majority of UK consumers to target.

And given the popularity of mobile and online banking offerings from traditional banks, the hurdle that neobanks will need to deal with first and foremost is convincing consumers to dip their toes in the water of digital-only banking.

Here are two key strategies neobanks could deploy to motivate customers to give them a try:

- Offer new sign-up incentives like perks or bonuses. Perhaps the most straightforward way to pull in customers is to offer a clear incentive to new sign-ups. This could be a promotional interest rate for deposits that is well above the market average (as Australian neobank Xinja is doing to attract deposits), or it could even be as drastic as a cash bonus deposited into newly opened accounts. A clear and present reward for signing up could be enough to get prospective customers' attention and get them to open an account, after which the neobank would have a chance to impress the client with its features and service. The drawback, however, is that incentives can rack up costs, a serious obstacle for neobanks as they already struggle with profitability almost universally.

- Reduce barriers to access existing account benefits. In many cases, neobanks will set deposit or transaction thresholds or other requirements that customers have to meet in order to access certain lucrative benefits. For example, US neobank Chime offers overdraft protection of up to $100 for users who direct deposit at least $500 per month into their account. If neobanks lower or remove such thresholds, it could help customers who have some curiosity or only want to experiment with a neobank to get a better feel for the full customer experience - and to do so without requiring a significant investment on their part. The downside to this approach would be that such thresholds offer neobanks a way to nudge customers to use their neobank account as their primary account, and primary account status is an elusive and important goal for neobanks.

Want to read more stories like this one? Here's how to get access:

- Sign up for Banking Pro, Business Insider Intelligence's expert product suite tailored for today's (and tomorrow's) decision-makers in the financial services industry, delivered to your inbox 6x a week. >> Get Started

- Check to see if you already have access to Business Insider Intelligence through your company, or inquire about access if you don't. >> Check If You Have Enterprise Access

- Explore related topics in more depth. >> Visit Our Report Store

- Current subscribers can log in to read the briefing here.

Next Story

Next Story Colon cancer rates are rising in young people. If you have two symptoms you should get a colonoscopy, a GI oncologist says.

Colon cancer rates are rising in young people. If you have two symptoms you should get a colonoscopy, a GI oncologist says. I spent $2,000 for 7 nights in a 179-square-foot room on one of the world's largest cruise ships. Take a look inside my cabin.

I spent $2,000 for 7 nights in a 179-square-foot room on one of the world's largest cruise ships. Take a look inside my cabin. An Ambani disruption in OTT: At just ₹1 per day, you can now enjoy ad-free content on JioCinema

An Ambani disruption in OTT: At just ₹1 per day, you can now enjoy ad-free content on JioCinema SC rejects pleas seeking cross-verification of votes cast using EVMs with VVPAT

SC rejects pleas seeking cross-verification of votes cast using EVMs with VVPAT

Ultraviolette F77 Mach 2 electric sports bike launched in India starting at ₹2.99 lakh

Ultraviolette F77 Mach 2 electric sports bike launched in India starting at ₹2.99 lakh

Deloitte projects India's FY25 GDP growth at 6.6%

Deloitte projects India's FY25 GDP growth at 6.6%

Italian PM Meloni invites PM Modi to G7 Summit Outreach Session in June

Italian PM Meloni invites PM Modi to G7 Summit Outreach Session in June

Markets rally for 6th day running on firm Asian peers; Tech Mahindra jumps over 12%

Markets rally for 6th day running on firm Asian peers; Tech Mahindra jumps over 12%